At the end of the 1999 season with the Mets, the team decided to cut bait with Bobby Bonilla but still owed him $5.9m at the time. Bobby’s agent, Dennis Gilbert, came to the Mets with an interesting proposition: hold on to your $5.9m, for now, and pay Bobby later down the road. Like…..twelve years down the road, starting in 2011.

The catch? In exchange for holding onto the roughly $6m dollars now, the Mets ownership (the Wilpons) would owe Bobby Bonilla $28.9 million, spread out over 25 years. Starting in 2011, the Mets would cut a check for $1,193,248.20 million every July 1st until 2035. Hence, Bobby Bonilla day! The way $5.9 million turns into $28.9 million is through compounding interest: Bobby agreed to wait on the payment of the money, but under the condition that his total payout would grow at an 8% interest rate over time.

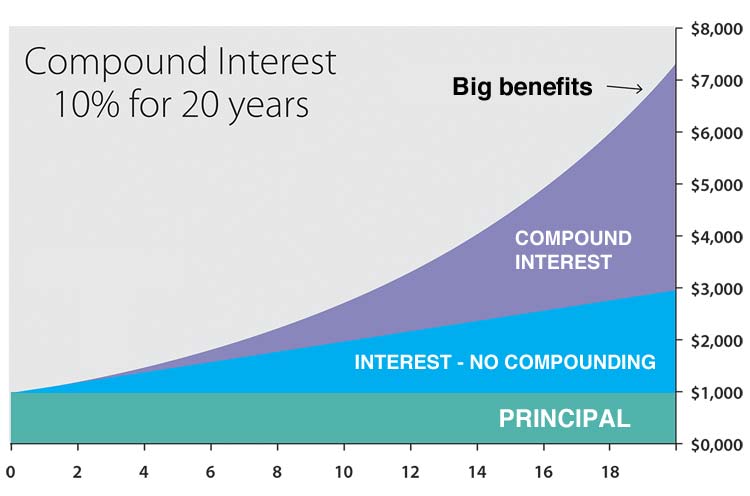

Think about that for a second….if you could guarantee an 8% rate of return on any investment for the better part of 35 years, would you do it? Of course you would! You should do that on any sizeable guaranteed rate of return, immediate payments needed withstanding. That is putting your money in an investment that has a 100% of growing. This gets to one of the most important pieces of investing, the same reason you save for retirement early: compound interest is your friend. If you save $1000 now and get 5% back, next year you have $1,050 – netting $50. Now that you have $1,050 with 5% back, the following year you now have $1102.50 – netting $52.50! Each year, you earn more and more, growing at an exponential rate.